Oil Shocks and the Bitcoin Network

Why the Revenue Side Is the Real Story

TLDR

- The direct link between crude oil prices and Bitcoin mining economics is weak.

- Countries where electricity prices correlate strongly with crude oil host an estimated ~6% of global hashrate. The other ~94% is largely insulated.

- The dominant risk is macro: geopolitical uncertainty depressing BTC price is more impactful than any oil-driven power cost move.

- USD hashprice hit a new all-time low of $27.89 per PH/s/day in February 2026 as BTC fell 23.8%, the deepest cycle drawdown yet.

- Over the trailing twelve months, rolling USD-denominated hashprice hedging has outperformed spot (FPPS) mining by up to +8.2%.

The Question

On February 28, 2026, the United States and Israel launched coordinated strikes on Iran targeting nuclear sites, military infrastructure, and its senior leadership. Within days, tanker traffic through the Strait of Hormuz — where roughly 20% of the world’s daily oil supply flows — collapsed to effectively zero, with ships anchored outside the strait rather than risk the passage. Drone strikes have spooked insurers into cancelling war risk coverage, triggering an insurance-driven shutdown of the world’s most critical energy chokepoint. Brent crude has since surged from $60/barrel in January to over $100, and is currently around $90 as U.S. President Donald Trump signaled that the war may be nearing its end. At this time of writing, the situation remains uncertain and volatile.

With oil around $100 and a geopolitical shock reverberating through global energy markets, what could this mean for Bitcoin mining economics?

The Supply-Side: Oil Barely Touches Mining Costs

Oil Powers Almost None of the Network

According to Cambridge Centre for Alternative Finance and Bitcoin Mining Council data, more than half the network runs on non-fossil sources, whereas crude oil as a direct fuel source for mining is essentially a rounding error. The more interesting question is whether oil price shocks transmit into electricity prices in countries where mining is concentrated.

Mapping Hashrate Against Grid Sensitivity

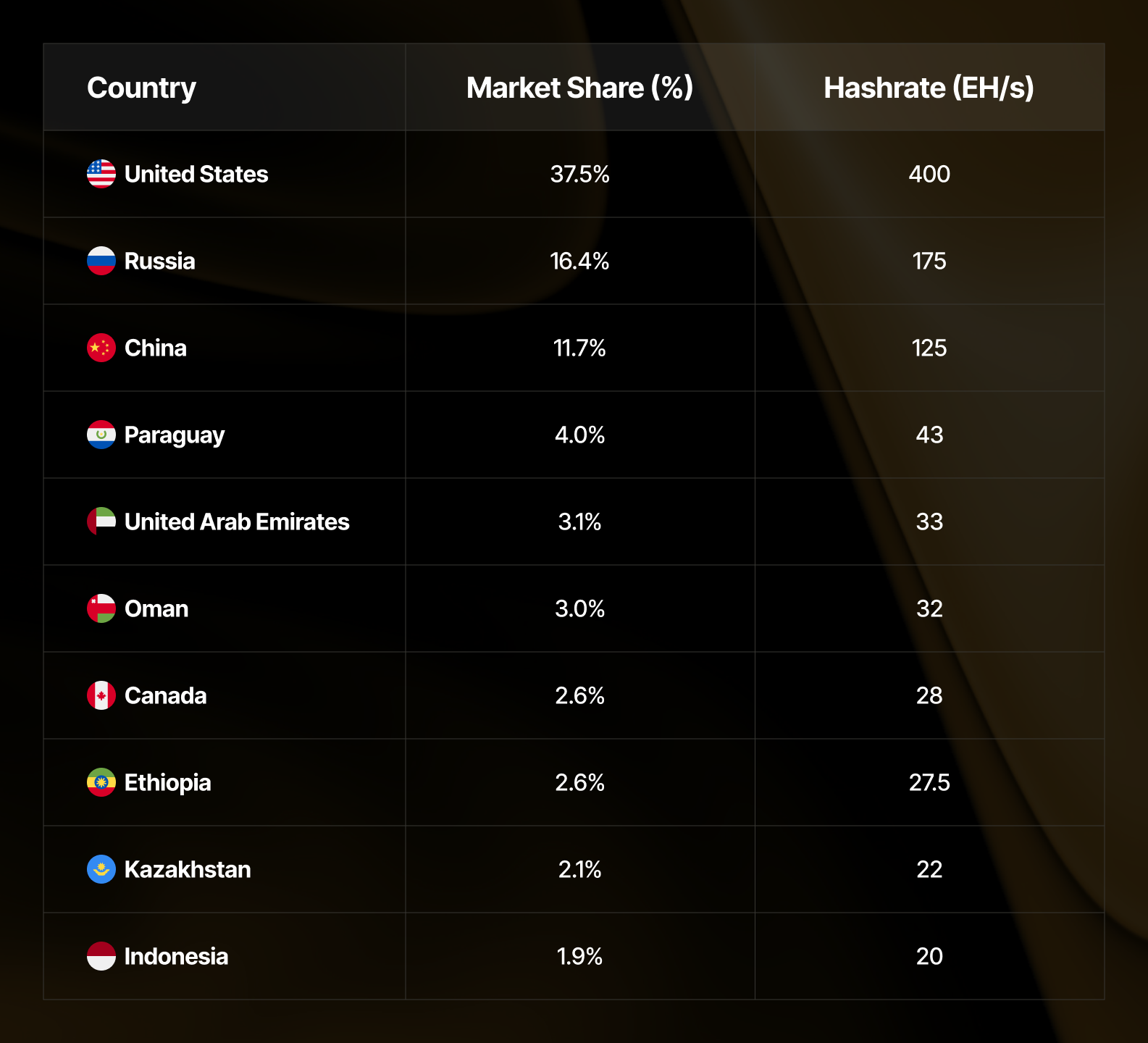

The latest Hashrate Index Global Hashrate Heatmap (Q1 2026) provides a clear picture of network geography. The top ten countries by hashrate:

The US, Russia, China, Canada, and Kazakhstan all operate power markets where electricity prices are driven by natural gas, coal, or hydro — not crude oil. Paraguay runs almost entirely on Itaipu hydroelectric. Ethiopia is +90% hydro. Norway, Iceland, Bhutan all run on hydro or geothermal. None of these grids are meaningfully sensitive to crude.

Even in markets where some relationship exists, the correlation between crude prices and US industrial electricity rates runs between 0.1 and 0.3 — statistically present, but practically marginal. Where it does transmit, it would also do so slowly: the pass-through from a crude price shock to grid electricity may take months through utility rate-setting cycles, blunting the near-term impact on mining costs.

The Exposed Cohort: ~6% of Global Hashrate

The genuinely oil-exposed countries in the heatmap are the Gulf states: UAE and Oman together account for roughly 65 EH/s, or about 6% of the network hashrate. These grids run primarily on natural gas derived from oil production, with electricity pricing that does track crude more directly than in the US or Russia.

Iran is estimated to hold another ~9 EH/s (0.8%). Smaller contributors like Kuwait, Qatar, and Libya bring the total crude-sensitive hashrate exposure to roughly 8–10% of the network.

Bottom line on supply-side: a sustained oil shock above $100/b would directly stress an estimated 8–10% of global hashrate. The remaining ~90% is either insulated by grid composition or faces indirect exposure such that it would likely not materially alter mining economics in the near term.

The Real Story: BTC Price Is the Variable That Matters

Cost Sensitivity Is Asymmetric

Even for the exposed cohort, a mining operation in the UAE running at $0.06/kWh with a fleet of S21 Pro’s (15 J/TH) has a hashprice breakeven around $22 per PH/s/day at current mining economics. Holding hashprice constant, A 33.3% rise in power costs from an oil shock would push that to $29 per PH/s/day — meaningful, but not catastrophic.

However, that same operation would be underwater with a 33.3% decline in USD hashprice.

February 2026's hashrate market data highlights this contrast. USD hashprice hit a new all-time daily low of $27.89 per PH/s/day on February 24, with a monthly average of $32.31, down 17.9% month-over-month. This was driven by a 23.8% decline in BTC price from $78,073 to $65,204.

BTC Price: Where Oil Actually Hits Mining

If oil at $100+ matters to Bitcoin miners, it is through the revenue side, not the cost side. A geopolitical shock severe enough to push crude above $100 (regional war, Strait of Hormuz disruption, major supply destruction) is also an event that may trigger risk-off positioning across global capital markets.

The transmission mechanism runs through inflation expectations and interest rates. A sustained oil shock above $100/b injects inflationary pressure as higher energy costs flow directly into CPI (through transport, manufacturing inputs, and utility bills). It also motivates central banks to respond by raising interest rates. Markets begin to adjust expectations, repricing for fewer or later rate cuts. This matters for Bitcoin: when real rates rise or rate-cut expectations get pushed out, capital rotates away from higher-volatility assets toward cash and short-duration instruments. The result is a macro-driven BTC revaluation, which has a direct impact on mining profitability through hashprice.

Bitcoin has increasingly behaved as a risk asset in acute stress periods. The current cycle’s deepest drawdown — a ~50% decline from the ~$126,000 October 2025 peak to ~$63,000 by late February — unfolded alongside broader macro uncertainty. Prior cycles confirm the pattern: the COVID crash took BTC down 62%, the 2022 macro tightening cycle produced a 77% drawdown from peak.

Applied to the question of oil shocks: the risk isn’t that miners in Texas pay $0.01/kWh more. The risk is that BTC reprices 20–40% lower as markets digest a geopolitical escalation, compressing USD hashprice at the same time. For miners, the question isn’t whether their power bill will rise. It’s whether their revenue denominator — BTC price — will hold.

The Trade: Hedging Hashprice in Volatile Markets

The Mechanism

In a geopolitical stress environment with oil elevated and BTC price under macro pressure, the case for USD-denominated forward selling is direct: lock in a hashprice today before a potential BTC price decline compresses it further.

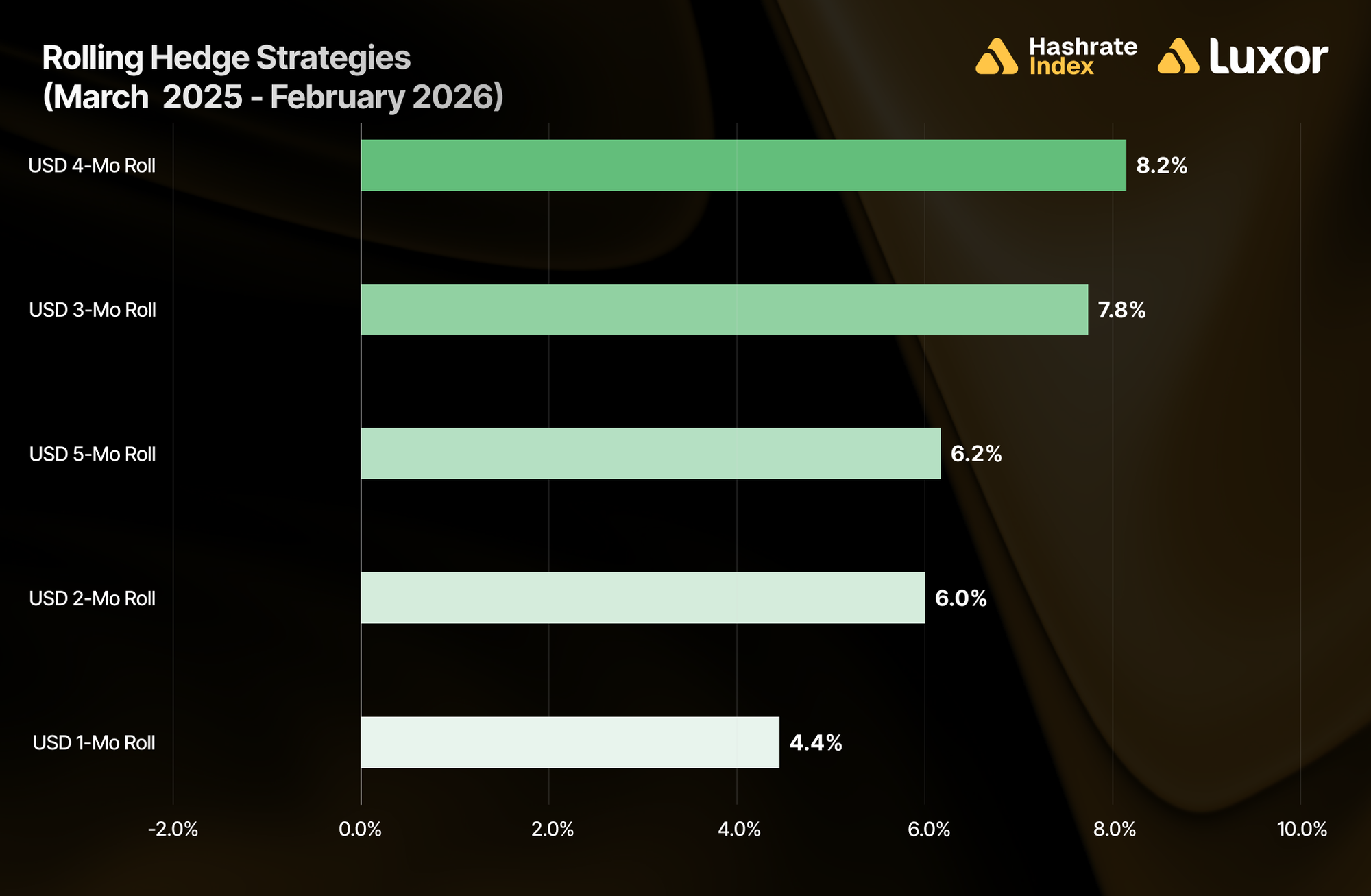

Trailing Twelve Months: The Performance Record

The chart below shows rolling hashprice hedging performance with Luxor’s OTC hashrate forward contracts from March 2025 to February 2026. Over the past year, rolling USD-denominated hedging strategies outperformed spot mining across the board. The strongest results came from 4-month (+8.2%) and 3-month (+7.8%) USD-denominated forward hashrate sales, which generally benefited from locking in a hashprice ahead of weak BTC price action, rising network difficulty, and low fee environments:

Who Should Be Hedging Now

The strongest candidates for selling hashrate forward in this environment:

- Marginal operators (20–24 J/TH fleets): At current hashprice, these operations are at or below breakeven. A BTC price decline pushes them into negative gross margins.

- Gulf-based miners: The ~6% of hashrate in oil-sensitive grids faces a double exposure scenario: rising power costs and potential BTC price decline from macro uncertainty. USD-denominated forward selling mitigates the revenue side of that risk.

- Operators with near-term CapEx obligations: Miners financing new machine deployments can benefit from selling hashrate forward to secure predictable cash flows and reduce credit risk, lowering their cost of capital.

Conclusion

The cost-side risk of high oil prices on bitcoin mining is narrow: roughly 8–10% of global hashrate sits in grids where electricity pricing tracks crude oil. The other 90% is on hydro, coal, gas, or nuclear grids where oil correlation is weak to negligible. A $100+ oil shock won’t take meaningful hashrate offline through cost pressure alone.

The real exposure is on the revenue side. A geopolitical shock severe enough to sustain oil above $100 is also the kind of event that moves BTC price, which is the variable that drives USD hashprice.

In a macro environment defined by geopolitical uncertainty and elevated oil, miners seeking predictable revenues can utilize USD-denominated hashrate forward sales to lock in a fixed hashprice ahead of a further potential BTC price deterioration.

As of early March, BTC is currently around ~$70,000 and USD hashprice is currently hovering around ~$30 per PH/s/day.

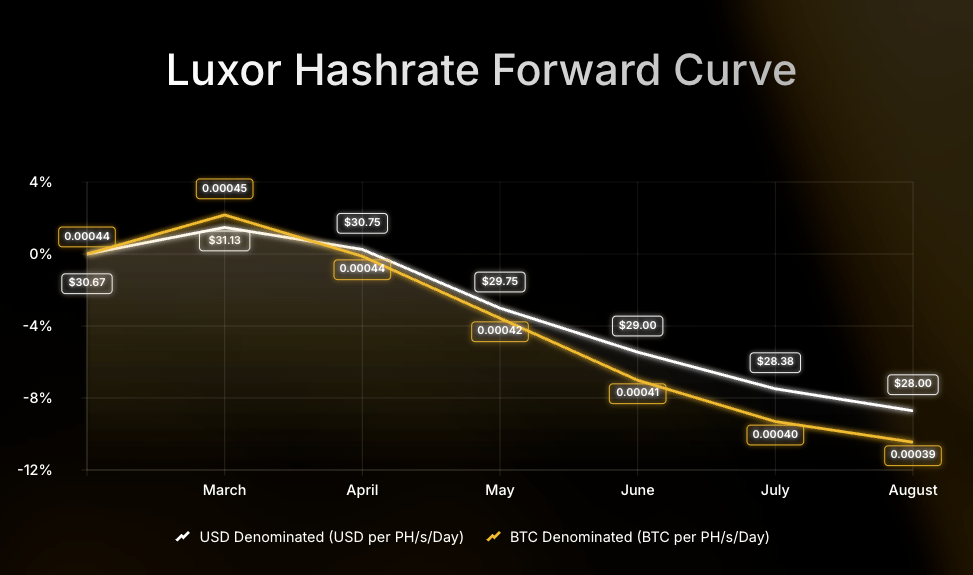

Looking Forward

Luxor’s Hashrate Forward Market is pricing in an average hashprice of $29.50 or 0.00042 BTC per PH/s/day over the next six months. Sellers can currently secure this hashprice while buyers have the opportunity to lock in the same hashcost through August 2026.

If you’d like to learn more about Luxor’s Bitcoin mining derivatives, please reach out to [email protected] or visit https://www.luxor.tech/derivatives.

About Luxor Technology Corporation

Luxor delivers hardware, software, and financial services that power the global compute and energy industry. Its product suite spans Bitcoin Mining Pools, ASIC Firmware, Hardware trading, Hashrate Derivatives, Energy services, and a Bitcoin mining data platform, Hashrate Index.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.

Hashrate Index Newsletter

Join the newsletter to receive the latest updates in your inbox.

{kind=link}